Fed-watching is foggy and frustrating, with predictions often wrong. Six insights help explain why. Understanding these six is step one to protecting yourself.

What fogs-up Fed-watching?

First, “Fed” is not a monolith. “Fed” is the Board of Governors of the Federal Reserve System plus twelve district banks. Each bank has a board of directors and appoints a president. The body that votes on monetary policy is the Federal Open Market Committee (FOMC). The FOMC is also not single-minded. The FOMC is individuals — the Governors, NY Federal Reserve Bank President and four rotating district bank presidents. Each member brings life experiences, professional school of thought on data and methods, motivations and objectives.

Second, “hawks and doves” is a bad way to describe FOMC members. For over 200 years, it has been a weak way to label foreign policy and worse for monetary policy. Stanford economist John Taylor helpfully characterizes FOMC individuals as monetary policy “rules-based” or not, similar to describing Supreme Court justices as Constitution “strict constructionists” or not.

Third, members have different policy trade-offs and views of how monetary policy tools actually work. For example, Janet Yellen is a labor economist; Stanley Fischer is the most international, born in Zambia and formerly Governor of the Bank of Israel; and Daniel Tarullo is an attorney focused on increasing regulation of banks.

Fourth, members focus on different data. This is why Fed-watching through economic news releases is difficult. Janet Yellen emphasizes labor slack. San Francisco FRB President Williams has an interest in natural interest rates. Members might be overlooking key data insights, especially on prices.

Fifth, the FOMC and markets created fog. For example, past interventions make measures such as natural interest rate difficult to see. Or, when a measure the FOMC seeks to move (e.g., interest rate) is already moving based on speculation of what the FOMC might do, it creates a loop like acoustic feedback through a microphone. In a way, these flow from the Heisenberg Uncertainty Principle.

Sixth, observers miss the FOMC process in their rush to “price in” the probability of the FOMC action. For insight into the process, a hat tip goes to Bob Eisenbeis, Vice Chairman of Cumberland Asset Management on his view of why there will probably be only two rate increases in 2016.

Tools of Fed-watching

Spectators eagerly watch FOMC press conferences, statements, minutes, staff reviews, dot charts and individual member speeches. Understanding causes of fog helps explain why people miss the message. For example:

- FOMC statements are quickly read for word changes. But, without understanding fog, traders are “surprised” – such as when as they under-appreciated international language for nine months.

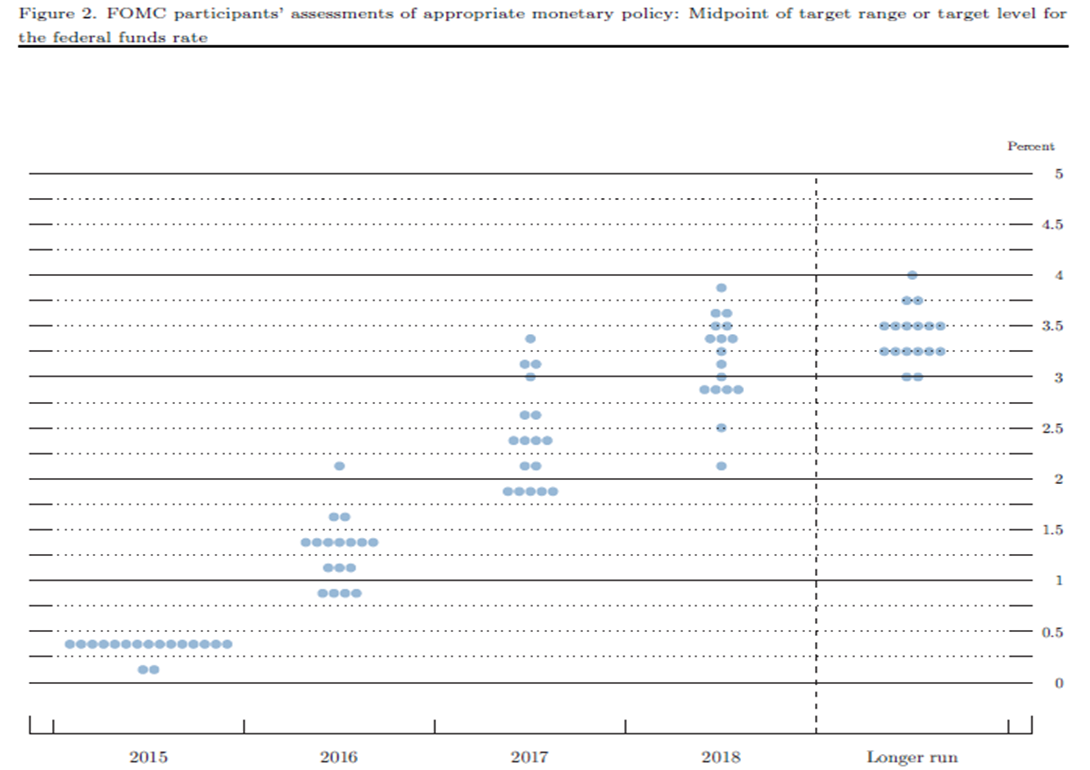

- FOMC dot charts reflect the combination of each member’s differences in: data focus, professional school of thought, good outcomes and how they believe a rate increase will actually transmit into an outcome. Thus, two members could put their dots in different places expecting the same economic outcome.

The Tough Test – “Why not?”

For analysts, it’s often tougher to explain why something did not happen than why it did. Here at Fed Dashboard & Fundamentals, “Cap and Lift” seems the best approach to interest rate increases. So why haven’t FOMC members voted this way?

Explanations above suggest FOMC members:

- Would benefit from more use company-level data and detailed product price-output data

- Are seeing dimly though the fog of prior interventions that obscured the natural interest rate

- Are struggling with the market feedback loop

- Would gain from immersion in today’s powerful influences such as technology, business model and value chain innovation, and managerial finance

Bottom Line

- Traders and investors listen differently to the FOMC

- Traders seek to out-guess other traders’ expectations of FOMC actions

- Investors seek FOMC actions for fundamental growth to position for higher real returns

- Investors have different opinions of whether a rate increase at a specific time is good or bad for specific industries and companies

- These differences make winners and losers in stock picking

- For stock picking, business model investing matters