Debt becomes most destructive – when, like a drug, more debt is needed to support sales and production. It’s worse when debt also bubbles financial asset prices.

After 1979, sales and production fell relative to debt

From about 1958-79, roughly constant was the ratio of Gross Domestic Product (GDP) to Nonfinancial Sector Total Liabilities at about 0.6.

In those decades, when people, businesses, and governments borrowed to invest in houses, productive capacity, or infrastructure, GDP increased proportionally.

Debt is helpful when incurred by people with comfortable debt to income ratios and with little threat to that income.

Then the relationship collapsed, more debt no longer proportionally increased GDP during the 1980s.

In the 1990s, the relationship stabilized, but at a lower ratio of about 0.45. From 1997 to 2009, the ratio again fell – debt contributed even less to GDP. Part of the reason is that debt had been used to buy houses. The debt is accounted for when incurred. But, the benefits are accounted for more slowly as ongoing housing consumption expenditures.

These falling ratios reflect a destructive aspect of debt. When the use of debt becomes destructive, debt grows, but productive capacity and sales don’t grow.

Excess debt hurts businesses because it is a fixed cost, regardless of sales. Excess debt hurts consumers when high rates combine with high debt service to choke off consumption and thus GDP. This painful, personal story is too common.

Zooming out, the national data is more like epidemic-level data. It takes more of the debt drug to support goods and services purchases. While individuals might be cut off from new debt, across the population, debt rises. Thus, the ratio falls. In addition, even good drugs can damage the digestive system, hurting people more.

To be clearer, consider key components of GDP. In the view below:

- Nonfinancial corporate businesses have been increasing their total liabilities relative to their production. These liabilities include commercial and industrial loans or, more recently, businesses using debt securities to buy-back shares to increase any per-share financial measure. We’ve discussed this previously in “Investors, be alert for these two credit trends” and “Don’t rebalance your portfolio without first checking these 3…”

- Personal Consumption Expenditures (PCE) relative to Household and Nonprofit Total Liabilities have been falling on a stunning exponential curve. More in our Consumer Credit section.

- As GDP is widely impacted by government debt, GDP is shown relative to combined federal, state and local (excluding pension liabilities) total liabilities. Since 2010, the ratio has been worse than at the end of World War II.

In short, the benefit of debt to enable sales and production has greatly diminished.

In short, the benefit of debt to enable sales and production has greatly diminished.

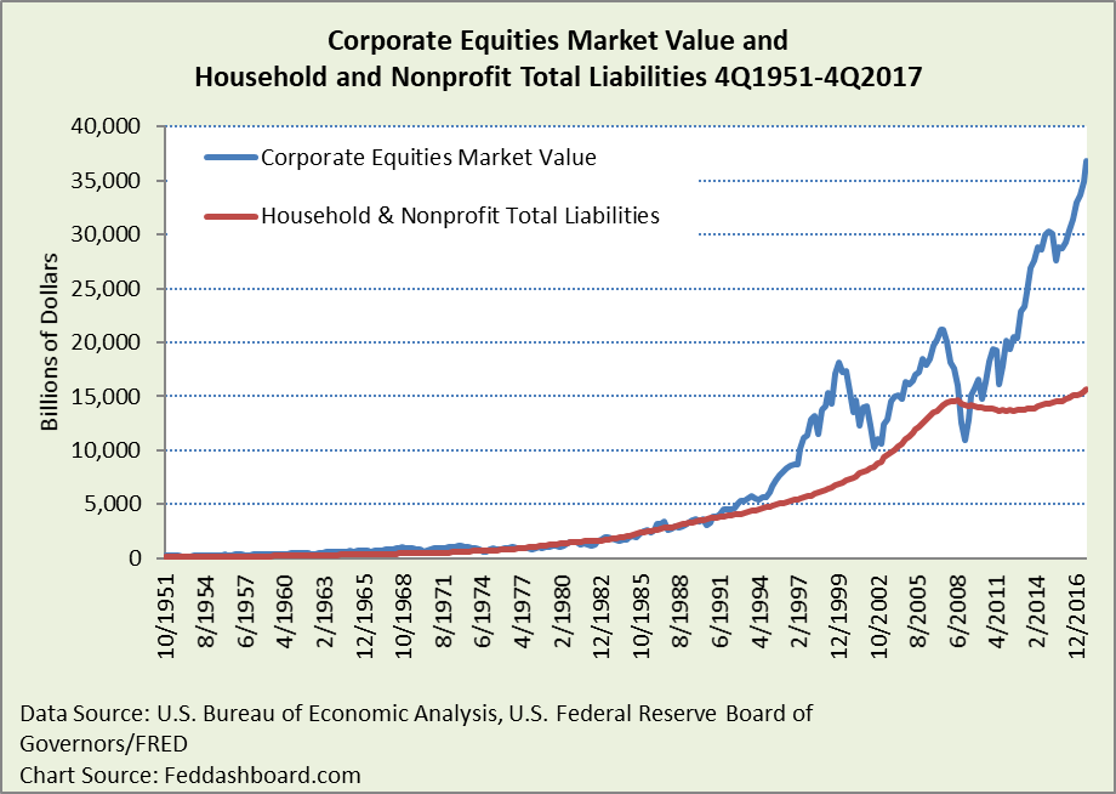

After 1974, Household and Nonprofit debt contributes more to financial asset price growth

The benefits of debt to GDP may have deteriorated, but debt still flows to corporate equity values. Since 1974, Household and Nonprofit Total Liabilities have been a dominant force in corporate equity market value.

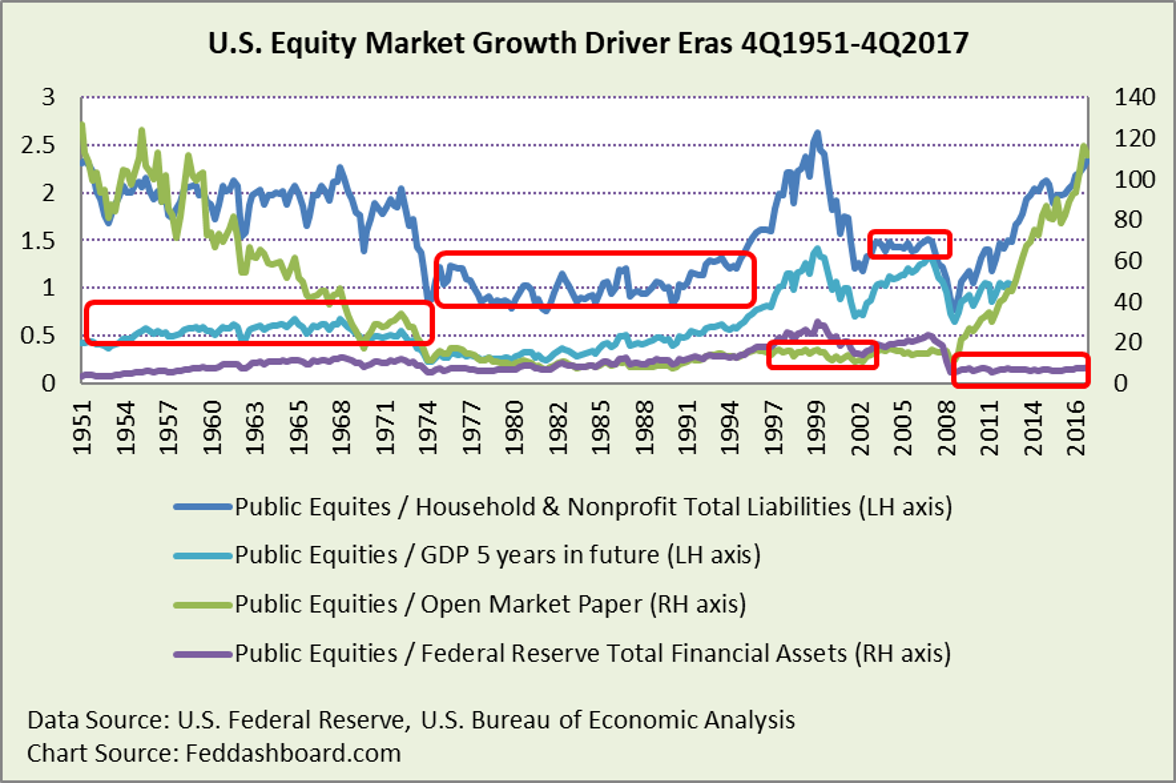

The exceptions to debt dominance include:

The exceptions to debt dominance include:

- Dot com-telecom bubble when investor speculation was a stronger driver (as proxied by commercial paper)

- Federal Reserve’s Large-Scale Asset Purchases (also known as quantitative easing, QE, or credit easing)

- Recently, Exchange-Traded Funds (ETFs) and inflows from the rest of the world have been supporting equity prices

The line chart below plots ratios. Thus, the flatter the line the more a factor in the denominator is consistently tracked by the numerator — the market value of public corporate equities.

With the Federal Reserve reducing its asset holdings, the relative influence of debt mathematically increases.

With the Federal Reserve reducing its asset holdings, the relative influence of debt mathematically increases.

Destructive big picture

- For people borrowing for houses, debt is risky if houses fail to appreciate. For people borrowing for short-lived goods, the debt drug tends to prey on the poorest. Both product purchase prices and interest rates transfer wealth to holders of equities. At a geopolitical level, this is no different from other countries lending to Americans, so indebted Americans can purchase from those other countries.

- For nonfinancial businesses, it means that higher returns on equity frequently come with higher credit risk. Yet, investors frequently fail to credit-risk adjust equity prices. As we’ve written in our Market Fundamentals section, different company business models produce strikingly different outcomes in sales, cash, and returns.

- For governments, it is a combination of the above plus “kicking the can” to future taxpayers

Debt dynamics within the global tech and trade transformation of falling global product costs and increasingly globalized financial markets

- Lower price level increases mean that debt can’t be “deflated” away

- GDP is increasingly demonetized due to falling goods prices, as we’ve written in our Exponential Tech This reduces both monetary policy options and tax revenue related to sales.

- Businesses, especially with less-advantaged business models, are increasingly vulnerable to credit risk from the above

- More people with lower incomes due to automation and “service humans” assisting robots worsens the household debt situation

- At a national level, the fight is to domicile companies with business models that generate high levels of cash to create policy options for governments – a fight the Chinese government clearly understands

For investors, this calls for an increased focus on business model-based investing and risk management

For governments and central banks, this means a policy rethink

To learn more about how to apply these insights to your professional portfolio, business or policy initiative, contact “editor” at this URL.

Data Geek Notes:

- Nonfinancial corporate business production is formally Gross Value Added (GVA), sometimes loosely termed as that sector’s GDP. The most recently released data is for 3Q2017.

- The discontinuities in the “Ratio to Total Liabilities” chart in 1975 are due to an accounting change for unidentified miscellaneous liabilities for nonfinancial corporate business