Growth in Japan’s compensation of employees hit a 20+ year high. Spending on durable goods and services also hit new highs. Yet, more focus is needed on three threats to Japan’s export engine and household health.

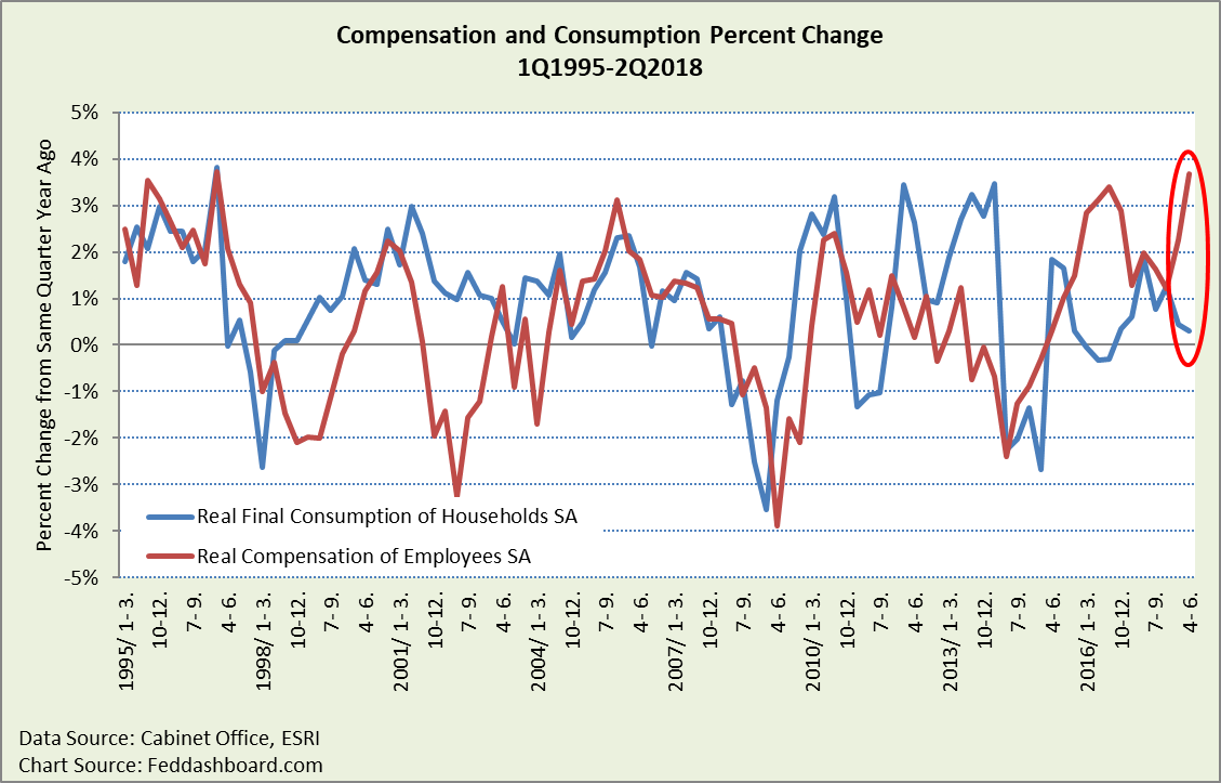

Growth in compensation and consumption continue Japan’s success story

Growth in Compensation of Employees (COE) is the highest in over two decades – since before the “Asian Flu” hit Japan in 1Q1997. We’ve known that since about 3Q2015 companies have been increasing payouts, although COE includes benefit contributions beyond immediately spendable cash. And, wage growth is shifting toward younger workers as seniority increases moderate. A hope is that rising wages for younger workers will lead to marriages and babies.

Shoppers have shown remarkable strength where it matters most – in largely discretionary durable goods since they rebounded in 2001 from the Asian Flu.

In 2Q2018, shoppers rebounded from a weak 1Q2017 to a historic high in durable goods. Services spending also rose to a new high. Yet, shoppers also showed restraint in semi-durables (such as clothing) and nondurables (such as food and energy).

- Bad news: Purchases of semi- and nondurables haven’t recovered to their 4Q2013 levels, prior to the shopping spree before the Value-Added Tax (VAT) increased 1 April 2014. By contrast, services recovered to the pre-VAT increase level in 1Q2015 and durables in 3Q2017.

- Backstory: Restraint in nondurables is partially due to energy conservation. Restraint in semi-durables is partially due to demographic changes, including fewer purchases of children’s and traditional clothing, as illustrated in “Good news: the Japanese economy is healthier – time to make babies.”

- Good news: Higher incomes combined with spending restraint creates historically high savings that could reduce household debt

In a myth that won’t die, the so-called Japanese “malaise” is not primarily about the individual shopper; it is more about demographics.

In a myth that won’t die, the so-called Japanese “malaise” is not primarily about the individual shopper; it is more about demographics.

- In population, since the Asian Flu recovery in 2001, Japan’s population has fallen by 0.1%. By contrast, the U.S. has grown by over 13%.

- Perhaps most striking is the compression of Japan’s population pyramid

- Growing aggregate consumption is more about growing babies than purchases per person

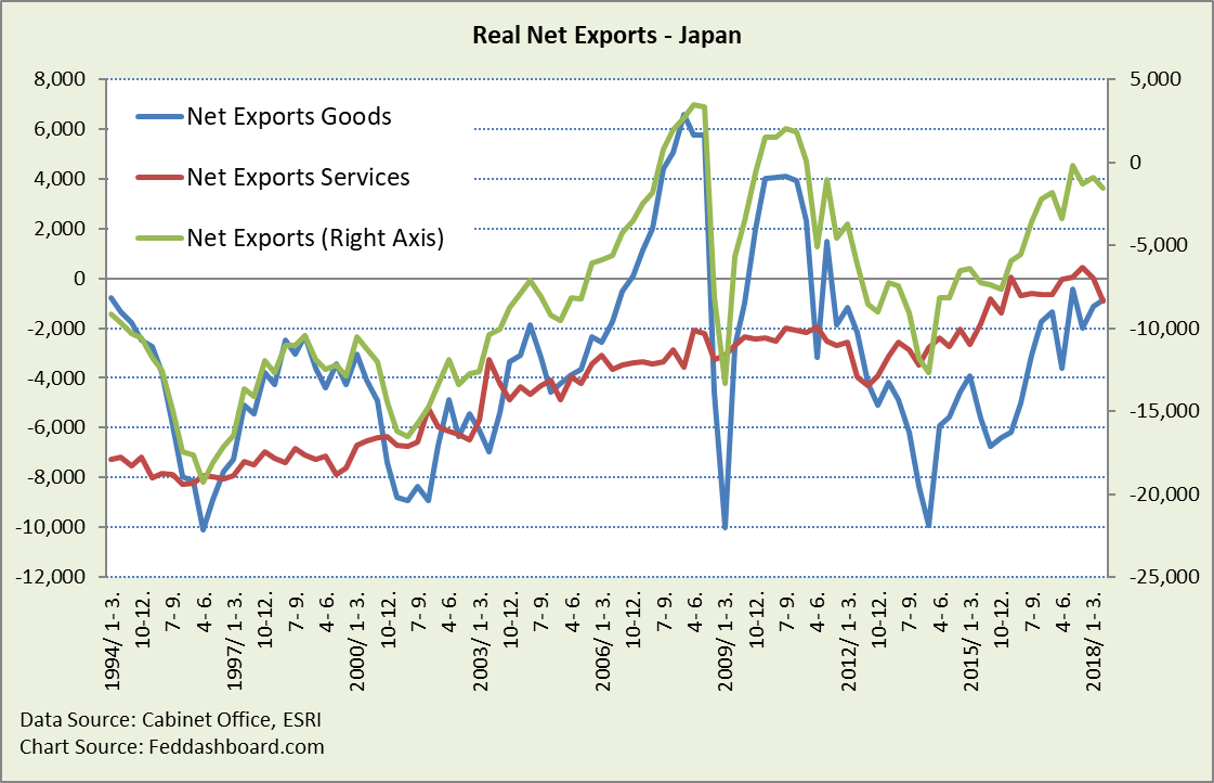

Debt, demographics, and tech weigh on Gross Domestic Product (GDP)

In 2Q2018, contributions to percent change in GDP:

- Help most came from Consumption of Households, Private Non-residential investment, and Net exports

- Hurt came from Private residential investment and Government investment

For forecasts and policy, dynamics matter:

- Government investment isn’t necessarily a villain as government decisions don’t reflect the same health as voluntary purchase decisions and help avoid debt and taxes

- Private residential investment in Japan will continue to be complicated by demographics including retirement savings, preferences for new housing, and tax disincentives to transferring private residential property across family generations

- Private nonresidential investment is shaped by falling costs of productive equipment. Global competition constrains margin growth. Recall, tech grows output measured in units but constrains output measured in currency. Think about mobile phones. At the extreme, this is the vanishing GDP problem.

What moved the needle in net exports? A boost in net exports of goods. That came from an upswing in exports of goods in 3Q2016 more than a change in imports.

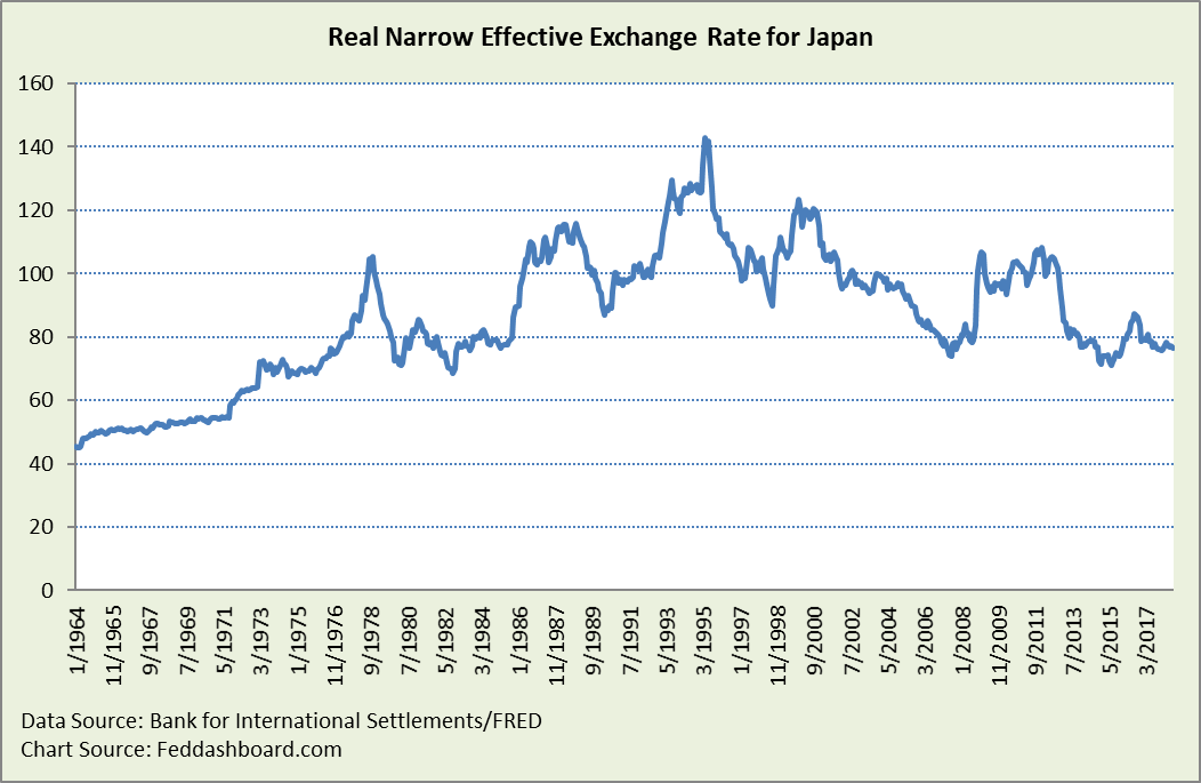

What does Japan’s export engine depend on? Underpinning growth are:

What does Japan’s export engine depend on? Underpinning growth are:

- Converting relatively costly raw materials into high-quality and/or lower cost exports

- Balancing exchange rates high enough to reduce the cost of imports and low enough to spur exports

- Rekindling momentum of W. Edwards Deming’s famed “Total Quality Management” together with honored Japanese management leaders who fostered lower cost and design innovation

Vitally, automation and improvement in management continue to cut cost. Yet, the spark of innovation isn’t as robust as in the past. Rising to the challenge, private sector improvements have been supported by the Government’s structural, corporate governance, and innovation initiatives, including the Government’s July 2017 new medical device approval process. Good news.

Japan’s real effective trade-weighted exchange rate is historically low

Today’s exchange rate means:

Today’s exchange rate means:

- Exports are cheaper to buyers elsewhere

- Imports are costlier to manufacturers and consumers. A weaker exchange rate imports inflation – if shoppers cut purchases, then GDP growth slows.

- If a company panicked due to the slide in 2018, then the lesson is to hedge or hedge better

Nonfinancial companies seeking to hedge are confronted by the usual need to guess goods and services trade. Since 2010, they need to better guess financial markets seeking safety in the Yen and the actions of central banks. Corporate treasury decisions are confounded by the Bank of Japan (BOJ) diverging from other central banks and disconnecting from Cabinet Office and financial market data.

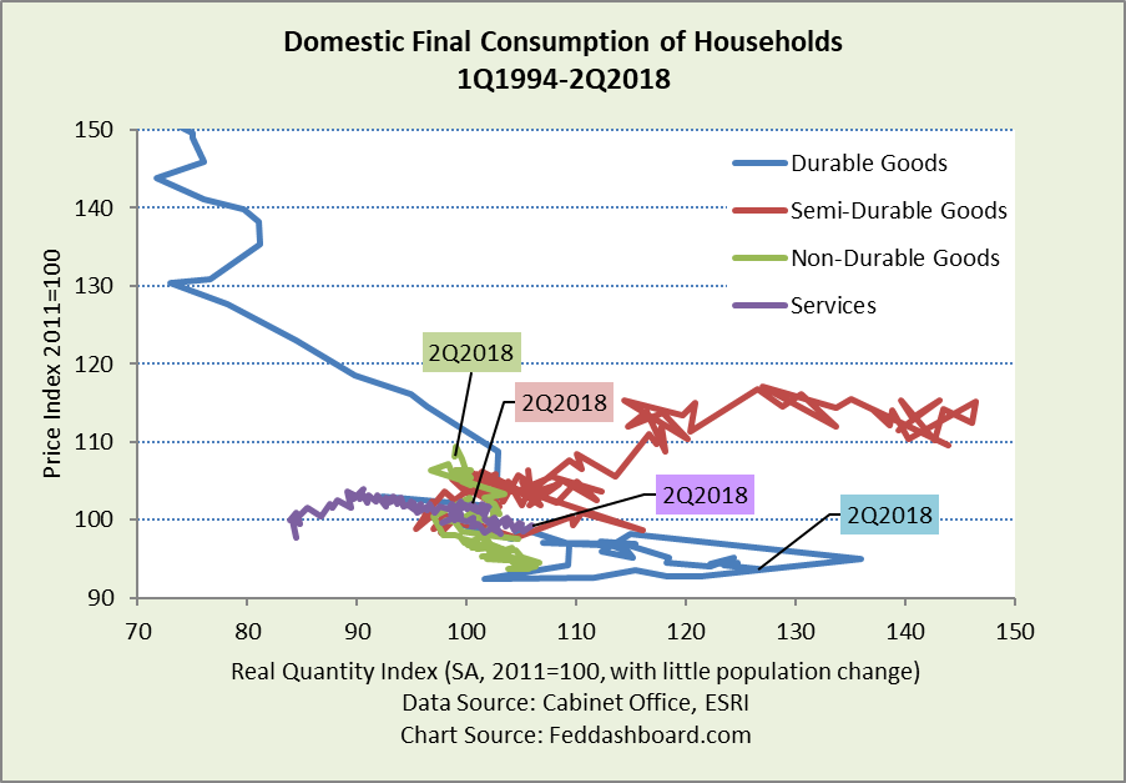

Shoppers buy more when prices fall

Meanwhile, prices continue their fall because of lower production costs, online shopping, global trade, and the Government’s structural reforms.

Chart Notes:

Chart Notes:

- Axes are unequal to zoom in on detail. Durables begins with a price index of 314 in 1994.

- Time generally moves from left to right with primary exceptions of 1) semi-durables that collapsed to a quantity index of 95 in 1Q2011 and 2) durables that collapsed to a quantity index of 112 in 3Q2014 after the VAT increase

Importantly, the 2Q2018 data points of the four categories also form a downward-sloping curve – shoppers buy more when prices fall.

Watch for dangers from actions that conflict with helpful policies

Good are policy initiatives to encourage babies, women at work, innovation, and corporate governance and structural reforms to cut cost and improve resource flexibility.

As the clock ticks to the VAT increase and Olympics, threats include:

- BOJ hurting GDP by sending excessively negative messages and pursuing higher prices in the face of the realities that 1) shoppers tend to cut purchases when prices rise, 2) the average shopper is already strong in durable purchases, 3) rising prices conflict with the Government’s reforms that tend to lower costs, including to promote exports, 4) household debt is still high, and 5) babies are needed

- Companies might not properly 1) balance exchange rate advantages and disadvantages without shifting production outside of Japan and 2) hedge

- The scheduled 2019 VAT increase given: 1) the last increase led to a cut in consumption greater than the Global Financial Crisis in 2007-9 and 2) sensitivity of shoppers to food and energy prices that played a role in the 1Q2018 spending pull-back

Acting now to harmonize policy can help Japan more easily achieve domestic objectives and strengthen its ability to project global stability as the largest market economy in Asia.

To learn more about how to apply these insights to your professional portfolio, business or policy initiative, contact “editor” at this URL.

Data Geek Notes:

- The “narrow” exchange rate with top trading partners is shown because it is a longer time-series than the “broad” rate. For more information see https://www.bis.org/statistics/eer.htm.

- Population data are from comparable time series of the World Bank